All About SPACs

Market Backdrop

Many readers may have seen a number of media articles on special purpose acquisition companies (SPACs) in recent months. SPACs are not new; however, they have become increasingly popular vehicles. I think much of this recent phase of popularity is due to the froth in the equity markets as a result of national government liquidity injections--specifically the Federal Reserve, Treasury Department and Congressional spending (Three Horseman Liquidity) in the US. One result of the extreme levels of market liquidity that has been "injected" into the economy has been (i) asset price inflation and (ii) stock market bubbles--not to mention everyday inflation for carbon based life forms.

Since Three Horseman Liquidity has flowed into the stock market, large capitalization technology and momentum stocks have risen as stimulus checks need to find a home and traditional market participants are riding the wave to make a profit as well. Today's correction in technology stocks notwithstanding--the goal is to increase asset prices across the board plain and simple. You should expect asset price inflation to continue regardless of market drawdowns for structural reasons to be discussed in a future article.

The SPAC Resurgence

With this backdrop in mind, why are SPACs making headlines lately? In short, a SPAC is a holding company that raises cash with the sole purpose to acquire a private third party business or merge with a third party business. Notable examples of prior SPACS are Virgin Galactic and Tesla competitor Nikola. As with most things involving the capital markets--SPACS are back because sponsors and some investors have been able to get rich using the vehicles in the recent past because of the increase in liquidity in asset markets.

Additionally, a greater number of SPACs are being established by former public company executives with the goal of acquiring a target in the executive's industry or a related industry. Reid Hoffman (Founder of LinkedIn) and Mark Pincus (Founder of Zynga) plan to raise $600 million through Reinvent Technology Partners (link). Moreover, it has become commonplace for private equity funds and hedge funds to serve as SPAC sponsors or partner with sponsors.

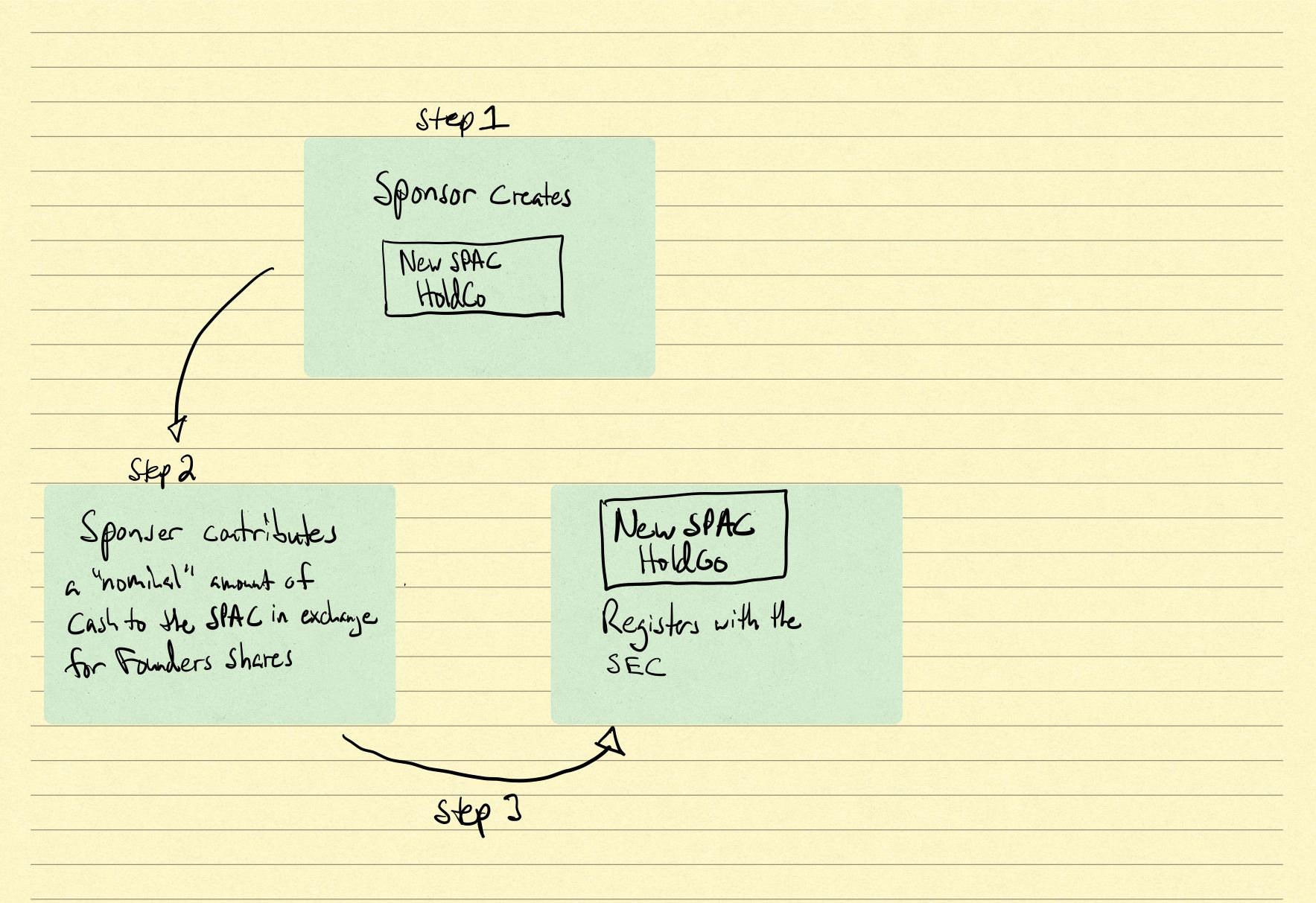

Example SPAC Structure (simplified for discussion purposes)

In step 1, the sponsor creates their SPAC and this entity is usually a Delaware company or a company formed in a tax efficient jurisdiction if the target company may be based overseas. In the overseas context, the jurisdiction is most commonly the Cayman Islands or British Virgin Islands.

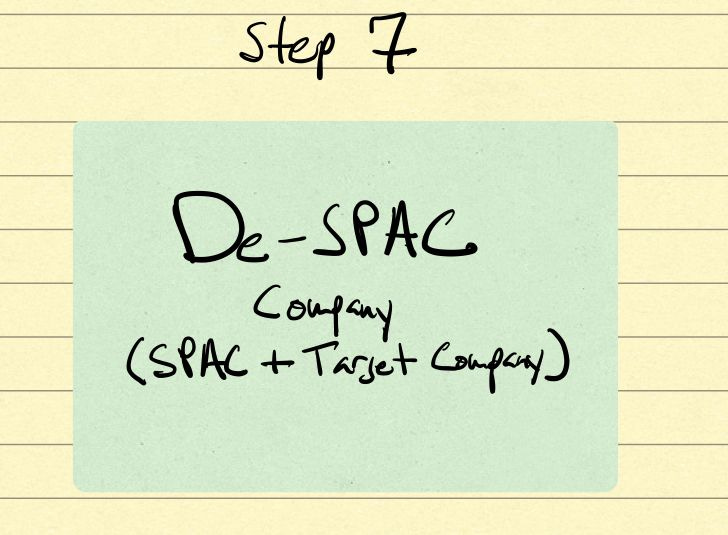

In step 2, the sponsor contributes a minimal amount of cash into the SPAC in exchange for "Founder Shares". The Founder Shares are a special class of shares that give the sponsor the right to receive a percentage of the De-SPAC company's IPO stock.

Step 3 is relatively straight forward in that the company registers as a SPAC and makes the relevant SEC filings detailing the purpose of the SPAC, timeline, deal terms, management team and business strategy of the SPAC.

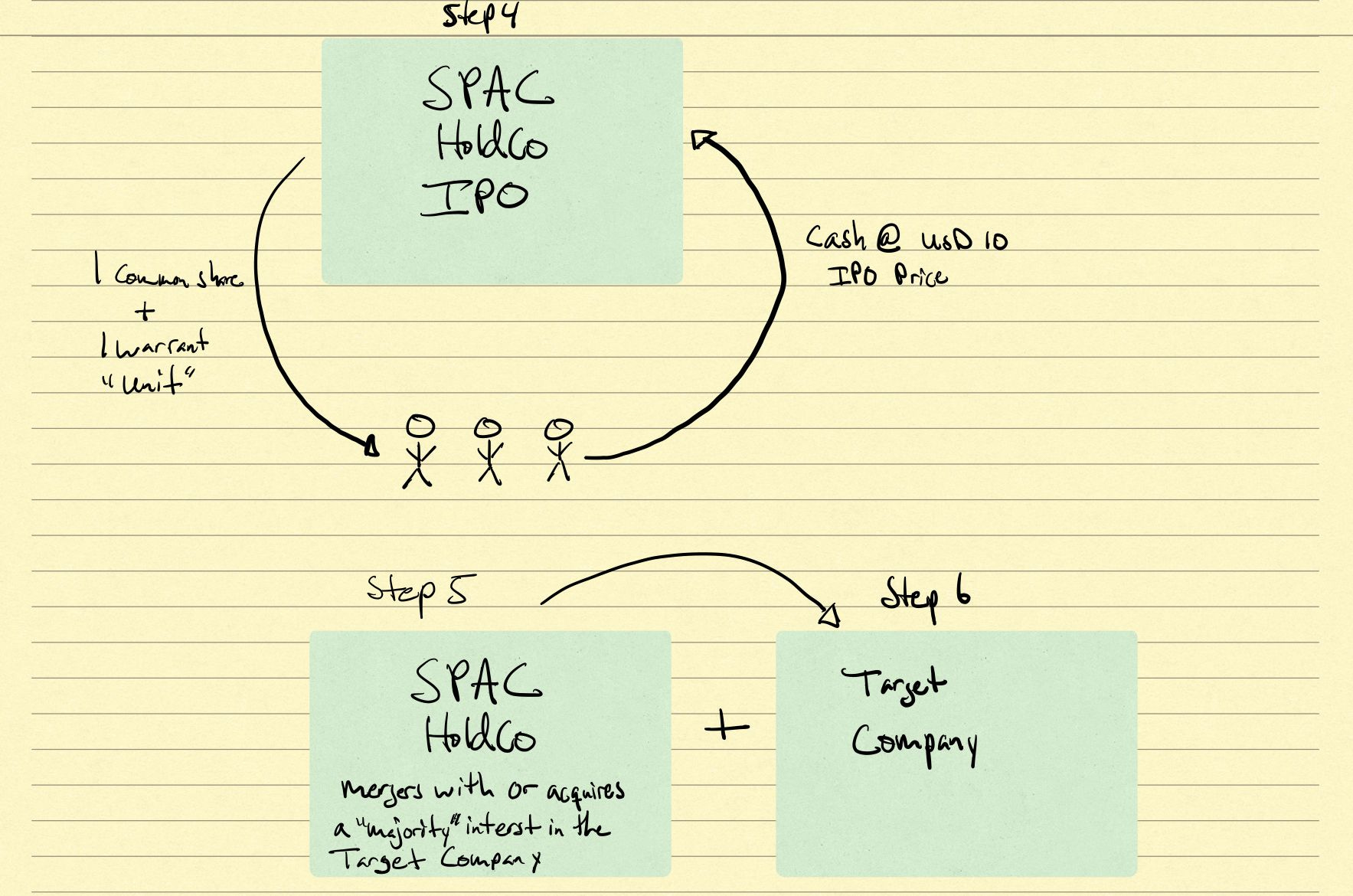

In step 4, after the SPAC IPO, the general public is able to buy shares in the entity before it seeks a target to acquire or does any business at all. This step represents the speculative risk and the financial opportunity in a SPAC. The "market" determines the movement in the stock price of the SPAC based on two primary factors (in theory because financial markets are complex systems).

First, the quality of the management team of the SPAC and its financial backers are critical to evaluate the potential success of the endeavor. Secondly, the ability of the SPAC to find a deal within its stated time horizon (which is normally a two year window or cash has to be returned to shareholders). Thirdly, the deal must be approved by the SPAC shareholders, target company shareholders and finally the SEC must provide the regulatory approval for the business combination.

The Economics of the public offering

Units versus Warrants

What is a Unit?

When the the SPAC offers units to the public, they are generally offered at a purchase price of USD 10 per unit (note the price will fluctuate since they are traded publicly) . A "unit" represents the value of one share of common stock and typically one warrant or a 1/2 warrant to buy an additional share of common stock in the De-SPAC company (a/k/a the post merger legal entity represented by the stock ticker).

Therefore, when you purchase a SPAC that is listed you will normally have the choice to buy the "unit" which represents both the common stock and the warrant together. Alternatively, you can purchase the common stock or the warrant separately because they trade under different ticker symbols.

What is a Warrant?

A warrant is right, but not an obligation, to buy a security, at a set price in the future, for a set period of time. With a warrant, the company creates a financial obligation for itself by setting aside a portion of its stock in the present to fulfill the possible future obligation to the buyers of the warrant seeking to exercise their right to buy the underlying common stock at the pre-determined price within the pre-determined period of time.

Let's use a hypothetical example:

1 Unit = USD 10 for each unit in the SPAC

1 Unit = 1 share of common stock + 1 warrant

1 warrant = the right, but not the obligation, to buy 1 share of common stock in the SPAC at X price until 2027.

If the warrants lists at USD 1, then the purchaser will be able to by the right, but not the obligation, to by the SPAC common stock at X price until 2027.

As you may have surmised, warrants can add a nice "pop" to a portfolio because they trade freely and the only cost is conceptually the price you pay for the optionality.

If you want to buy 500 warrants you will only need to "risk" USD 500 and if the underlying stock price does not reach X price by 2027, then the warrant out of the money and worthless. However, if the stock price is >X then the warrant is "in the money" and you can lock-in the right to buy more shares of the company in the future with a low up front price today.

Additionally, if the underlying stock drops or goes to zero you can only lose the total value you have paid for the warrants and not the value of the underlying shares.

I think the above is sufficient for now--more on this topic in future articles.

Finally, SPACs will often enter into agreements with third parties such as private equity funds and hedge funds to provide additional financing for the De-SPAC transaction. When a private equity fund enters into a financing agreement with a SPAC it is often called a private investment in public equity (PIPE) and happens at the same time as the business combination. The purpose of the PIPE is to minimize the risk that investors change their minds on the deal and seek to redeem their investment before the business combination can occur and to shore up the capitalization of the company.

In conclusion, this article is meant to serve as a primer for understanding the SPAC structure as a foundation for analyzing a SPAC transaction without referring to the nuts and bolts mechanics herein.

I hope you found this article useful.