What Does Singapore Tell Us About the Future of Central Bank Digital Currencies?

Key Takeaway: Governments around the world realize the pending irrelevance of the legacy banking systems resulting from broad based stablecoin and digital asset adoption. The policy grappling is centered around (a) whether or not to preserve a role for the legacy banking system, as a de facto arm of the state, and (b) if not, to allow for a managed transition to something else that is also under state control visa vi central bank [MAS] control.

Background

In the December 5th edition of my weekly newsletter, I highlighted for readers the recent spate of global central bank innovation hubs that have come online around the world from London to Singapore.

Money is, in the end, a social convention that can be very fragile under stress (Cunliffe, 2021).

In this piece I want to focus on a recent report from the Monetary Authority of Singapore (MAS) with a specific emphasis on their analysis and conclusions regarding retail focused Central Bank Digital Currencies (CBDCs).

Introduction

In this article, I will delve into the conclusions of the MAS and why I believe they layout a roadmap for similarly situated financial hubs and potentially the United Kingdom and USA. Let's start by looking at the MAS' rationale for conducting this deep dive analysis as they state directly:

It may be challenging for regulation and taxation alone to carry the full burden of stemming the adoption of foreign digital money instruments. Such measures may be inadequate if foreign currency denominated instruments truly offer an option that is desired by consumers and firms but unavailable in the domestic monetary system.

Key Conclusions of the MAS

One implication of the digital revolution is that the relevance of cash as a means of payment is diminishing.

The market structure of payments may undergo a fundamental change.

The ongoing digital acceleration globally is also uniquely marked by the emergence of new forms of digital money.

The central bank community has been considering a response to these developments by the issuance of a retail CBDC.

A retail CBDC would preserve the relevance of generally-accessible central bank money as the economy digitizes. As a public digital payment alternative, it would help safeguard consumer and merchant interests as commerce moves further online.

A retail CBDC would go a step further by establishing a universally accepted digital medium of exchange in Singapore.

MAS assesses that a retail CBDC that is elastically supplied and universally accessible just like cash is today could impact credit creation and, more broadly, financial and monetary stability in Singapore.

The MAS' preliminary assessment is that with appropriate regulatory safeguards, financial stability risks posed by a retail CBDC are likely manageable. My read on this assessment is that the subtext is one of caution given the new variables a retail CBDC would introduce into the implementation of monetary policy.

I find it most interesting that the MAS ultimately concluded now is not the time to roll out a retail CBDC; however, they hedged their conclusion by saying that development on a retail CBDC should continue to be able to quickly launch such a product based on market developments. The MAS has provided a key lens into the thinking of all central banks on this core point, in my opinion, because of the complexity in structuring and launching such a project they are effectively advocating for a "rolling start" to use a motorsport term such that the central bank is not left behind by technological change.

Conclusion

In the world of CBDCs, I think we are going to enter the age of competitive monetary policy being used as a means to attract capital because any efforts to limit the free movement of capital cannot be hidden from the market in this new era.

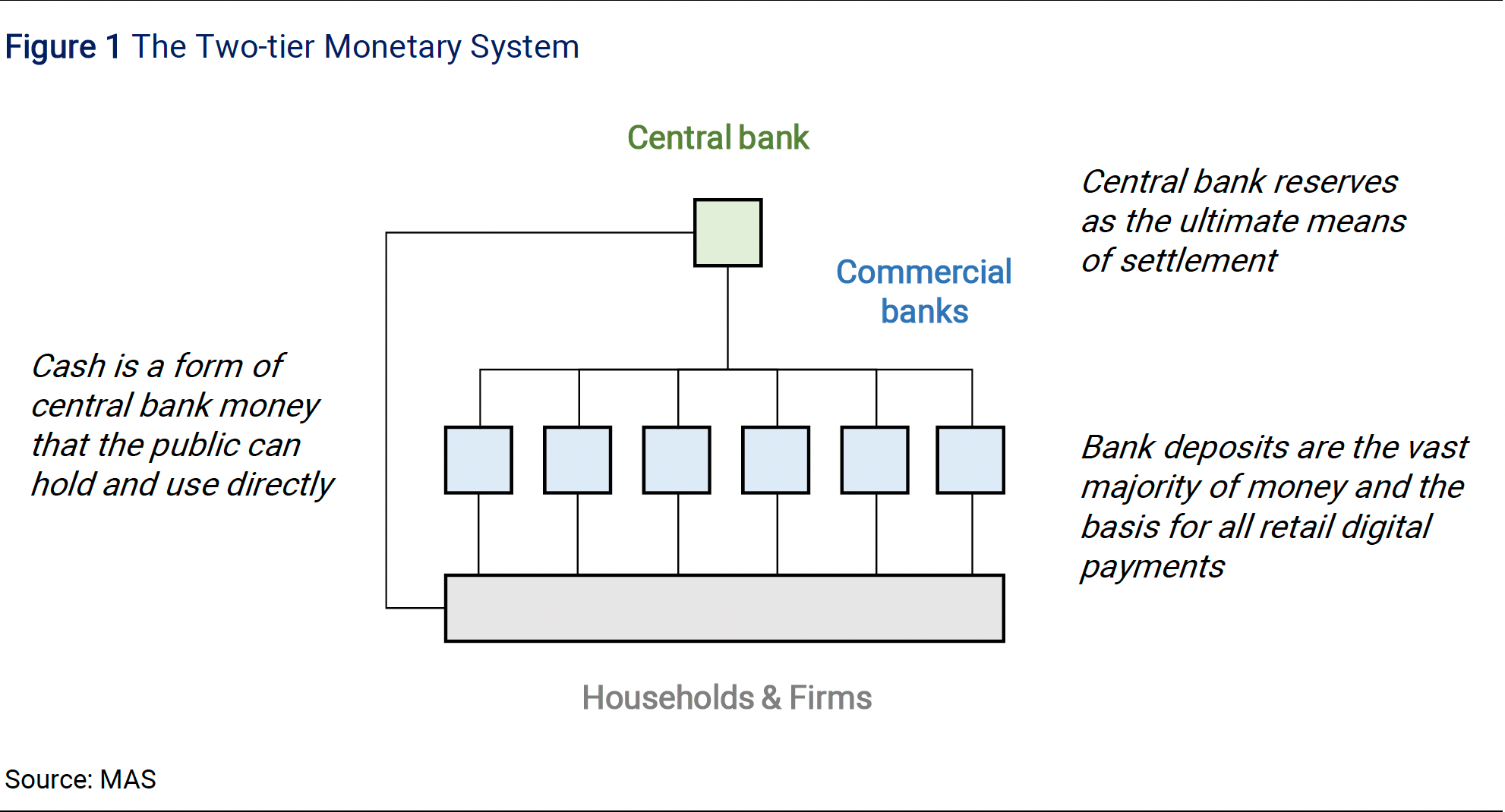

As the MAS notes in the graphic above, market participants could more easily vote with their "keystrokes" to exit a currency system all together if the local monetary policy is perceived as harming the currency (absent China style regulatory and capital controls). See the Turkish Lira or Argentinian Peso for real world examples.

In this new multi currency and multi polar world, similar to 18th century banking, the brand of a nation could very easily rest on the status of that nation's finances--- judged by the value of the currency with citizens able to exercise their vote of confidence in central bank policy. While this may exist today, I would argue the world of centrally coordinated currency only allows for the illusion of a free market or free floating currency. In reality every nations currency is heavily managed absent shocks which have tended to be quickly managed by G20 nations. Retail CBDCs, in the context of stablecoins and digital assets generally, pose new challenges along with opportunities for the central bank to exert more control over their currency.

The core concern of the MAS in the context of a retail CBDC discussed in this particular paper is (i) the lowering of the barriers for citizens to easily switch to or adopt another nations CBDC and (ii) the lowering of friction in the financial system generally that may make bank run scenarios easier when retail customers can more easily opt out of retail banking cash deposits and into a retail CBDC was a direct central bank claim.